Thursday, June 24, 2021

By Andy Nielsen

In a legislative session dominated by the biennial budget and pandemic response, Indiana lawmakers took an important step to strengthen our state’s social safety net for many Hoosiers across the state. House Enrolled Act 1009 increased the state’s Earned Income Tax Credit (EITC) from nine percent to ten percent of a taxpayer’s federal EITC, which had been largely untouched since 2011. Many thanks to our lawmakers for recognizing the effectiveness of this tried and true tool to help combat poverty in Indiana.

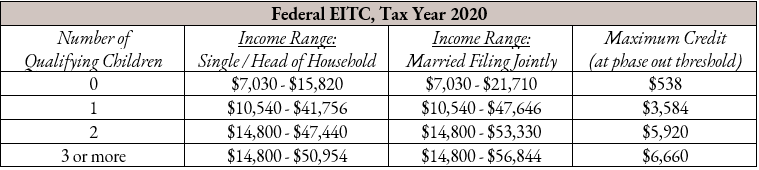

The federal EITC was created in 1975 as a tool

to incentivize work, boost earnings, and combat poverty. Eligibility and the

amount of the credit are a function of a taxpayer’s earned income, filing status,

and the number and age of children claimed on the tax return. Simply put: the

more you (and/or your spouse) work, the higher the credit, and once you earn a

certain amount, the credit begins to phase out. Have kids? Then you may receive

a larger credit.

The federal credit phases out at a higher income for married

couples filing jointly compared to individuals filing single or head of

household. However, the maximum credit is determined by the number of children

(under age 19 or 24 if full-time student and must have a valid SSN) claimed on

the return and whether or not the filer is single or married. The table below

illustrates these differences. Income ranges provide the minimum earned income

to receive the maximum EITC and the maximum amount where credit is zero (completely

phased out).

Source: Congressional Research Service (Link)

The federal EITC has been extremely effective at combating

poverty and is quite popular. In 2018,

the credit lifted approximately 5.6 million people out of poverty – including

about three million children. Data from the Internal Revenue Service

(IRS) for tax year 2019 demonstrates the credit’s popularity with about 25

million individuals and families nationwide receiving an average EITC of around

$2,461, including 515,000 Hoosiers with an average credit of $2,424. Unfortunately,

only 78% of

eligible taxpayers (79.8% in Indiana) claimed the federal tax credit in 2017. To put

this in perspective, nearly 135,000 additional Hoosiers were eligible but did

not claim the credit – that’s over $324 million gone unclaimed.[1]

One of the more important features of the credit is that it is

fully refundable, meaning the "unused" portion of the credit is recouped through

a refund at tax time. A quick refresher on tax credits. Unlike tax deductions

that lower taxable income, tax credits offset tax liability dollar-for-dollar.

Say you owe $2,000 in taxes and have a $2,400 credit. If the credit is

refundable, your tax liability is reduced to $0 and you receive the remaining

$400 of the credit as a refund on your return. If the credit is non-refundable,

the remaining $400 is left on the table. Refundability ensures the credit is

fully realized by low-income taxpayers who may reduce their tax liability to

zero through other credits or deductions.

In 1999, Indiana followed the federal government’s lead by

creating its own EITC. While the credit was modified several times and remains

decoupled (stay tuned for future blog post) from its federal counterpart, the

state credit is still an

important tool for Hoosiers. Like the federal EITC, Indiana’s credit is

fully refundable, making it among the

most effective and targeted tax reduction strategies to help offset regressive

state taxes. According to an analysis provided by the Institute

on Taxation and Economic Policy (ITEP), recent

changes (effective tax year 2022) made to Indiana’s EITC in the 2021 Legislative Session will

provide a tax cut to 13 percent of Hoosiers (see table below). Again, this is

an important change and a moment to celebrate the legislature’s efforts towards

a stronger social safety net, but we need to keep up the momentum.

Looking ahead, Indiana needs to focus even further on using the tax code to strengthen Hoosier households and families. Given the substantial changes made to the federal EITC, Indiana lawmakers should create parity between the federal and state credits, which would be a critical step towards further improving the livelihoods of our most vulnerable fellow Hoosiers.

[1] Author’s calculations using participation rates and individual income and tax data from 2017 IRS data.